RSS Feed

RSS Feed

January 3rd, 2018

January 3rd, 2018  Awake Goy

Awake Goy Central banks are now trapped.

In a nutshell, central banks are promising to “normalize” their monetary policy extremes in 2018. Nice, but there’s a problem: you can’t “normalize” markets that are now entirely dependent on extremes of monetary stimulus. Attempts to “normalize” will break the markets and the financial system.

Let’s start with the core dynamic of the global economy and nosebleed-valuation markets: credit.

Modern finance has many complex moving parts, and this complexity masks its inner simplicity.

Let’s break down the core dynamics of the current financial system.

The Core Dynamic of the “Recovery” and Asset Bubbles: Credit

Credit is the foundation of the current financial system, for credit enables consumers to bring consumption forward, that is, buy more stuff today than they could buy with the cash they have on hand, in exchange for promising to pay principal and interest with their future income.

Credit also enables speculators to buy more assets than they otherwise could were they limited to cash on hand.

Buying goods, services and assets with credit appears to be a good thing: consumers get to enjoy more stuff without having to scrimp and save up income, and investors/speculators can reap more income from owning more assets.

But all goods/services and assets are not equal, and all credit is not equal.

There is an opportunity cost to any loan (i.e. credit), as the income that will be devoted to paying principal and interest in the future could have been devoted to some other use or investment.

So borrowing money to purchase a product or an asset now means foregoing some future purchase.

While all products have some sort of payoff, the payoffs are not equal. If I buy five bottles of $100/bottle champagne and throw a party, the payoff is in the heady moments of celebration. If I buy a table saw for $500, that tool has the potential to help me make additional income for years or even decades to come.

If I’m making money with the table saw, I can pay the debt service out of my new earnings.

All assets are not equal, either. Some assets are riskier than others, with a less certain income stream or payoff. Borrowing to buy assets with predictable returns is one thing, buying assets with highly speculative returns is another; regardless of the eventual result of the investment, the borrower still has to pay interest on the debt, even if the speculative investment goes bust.

The basic idea here is the loan is based on collateral, that there is something of value that is anchoring the loan above and beyond the borrower’s ability to pay principal and interest.

The classic example is a house: the lender issues a mortgage based on the market value of the house, i.e. what it can be sold for should the buyer default on the mortgage and the lender has to sell the collateral (the house) underpinning the loan.

The value of the collateral is obviously contingent on the market; the value of the house goes up and down depending on supply and demand, the availability and cost of credit, and so on.

If a lender loans me $500 to buy a new table saw, and I default on the loan, the table saw is the collateral. Unfortunately for the lender, the market value of the used tool is perhaps $250 at best. So the lender loses $250 even after repossessing and selling the collateral.

If the lender loaned me $500 to buy champagne and I default, there is no collateral at all; the loan was based solely on my ability and willingness to pay principal and interest into the future.

When I say that all credit is not equal, I’m referring to the creditworthiness of the borrower.

Lenders make money by issuing credit to borrowers. The incentives are clear: the more credit they issue, the higher their income.

Given this incentive, it’s easy to convince oneself that a marginal borrower is creditworthy, and that a speculative investment is a safe bet.

This is especially true if the government guarantees the loan, for example, a home mortgage. With the government guarantee, there’s no reason not to take a chance on a marginal (risky) borrower buying a marginal (risky) house.

If we take some home mortgages and bundle them into a mortgage-backed security, we can sell the future income stream (i.e. the payments made by the borrowers in the future) as securities that can be sold worldwide to investors. I can make risky loans, skim the fees and pass the risk onto global investors.

All this debt is now considered an asset to investors.

There’s one last feature of credit: liquidity. Liquidity refers to the pool of credit available to refinance or roll over existing debt. If I’m having trouble paying my credit card, for example, and there’s plenty of liquidity in the credit system, I can obtain a larger line of credit and borrow enough to pay my monthly principal and interest on the existing debt.

If I can refinance my existing debt at a lower interest rate, so much the better.

Credit can be issued by private-sector lenders to private-sector borrowers, or by public-sector central banks to private-sector lenders. Central banks can buy public and private debt (government and corporate bonds, mortgages, etc.), effectively transferring debt from the private sector to the public sector.

These are the basic moving pieces of the credit expansion that has fueled both the “recovery” and the reflation of asset valuations, which have now reached historic extremes.

The Current (Flawed) Logic We’re Pursuing

In response to the Global Financial Crisis (GFC) of 2008, central banks lowered interest rates to near-zero to boost private-sector lending, and increased liquidity to enable private-sector lenders and borrowers to refinance existing debt and generate new credit.

They also bought assets: government bonds, corporate bonds and in some cases, stocks via ETFs (exchange traded funds).

The goal here was to prop up the collateral underpinning all the debt. If liquidity dried up, consumers and enterprises would default, handing lenders catastrophic losses, as the crisis had crushed the market value of the collateral that lenders would have to sell to recoup their losses.

And so central banks pursued heretofore unprecedented policies aimed at goosing private-sector lending and borrowing while boosting the markets for stocks, bonds and real estate—the collateral that supported all the debt that was at risk of default.

All this low-cost and easily available credit, coupled with the central banks’ public messages that they would “do whatever it takes” to restore credit mechanisms and reflate the private-sector markets for stocks, bonds and real estate, worked: credit expanded and markets recovered, and then soared to new highs.

While these policies accomplished the intended goals, boosting both new credit and asset valuations, they also generated less salutary consequences.

By lowering interest rates and bond yields to near-zero, central banks deprived institutional owners who rely on stable, high-yielding safe investment income—insurers, pension funds, individual retirement accounts, and so on—of exactly what they need: safe, stable, high-yield returns.

In this “do whatever it takes” environment, the only way to earn a high return is to buy risk assets—assets such as stocks and junk bonds that are intrinsically riskier than Treasury bonds and other low-risk investments.

The Stark Conundrum We Face

Central banks are now trapped. If they raise rates to provide low-risk, high-yield returns to institutional owners, they will stifle the “recovery” and the asset bubbles that are dependent on unlimited liquidity and super-low interest rates.

But if they keep yields low, the only way institutional investors can earn the gains they need to survive is to pile into risk assets and hope the current bubbles will loft higher.

This traps the central banks in a strategy of pushing risk assets—already at nose-bleed valuations—ever higher, as any decline would crush the value of the collateral underpinning the titanic mountain of debt the system has created in the past eight years and hand institutional owners losses rather than gains.

This conundrum has pushed the central banks into yet another policy extreme: to mask the rising systemic risk created by asset bubbles, central banks have taken to suppressing measures of volatility—measures than in previous eras would reflect the rising risks of extreme asset bubbles deflating.

In Part 2: So What Comes Next & How Can We Prepare For It?, we’ll ask: how does this resolve? Can central banks raise rates without popping the bubbles the system needs to remain solvent? Or can they keep yields near zero and keep pushing asset valuations higher for years or decades to come?

Or is this all much more likely to end in a massive financial/currency crisis? One characterized by default and liquidation of America’s high-fixed-cost, heavily indebted households and enterprises that have only stayed afloat by borrowing more money?

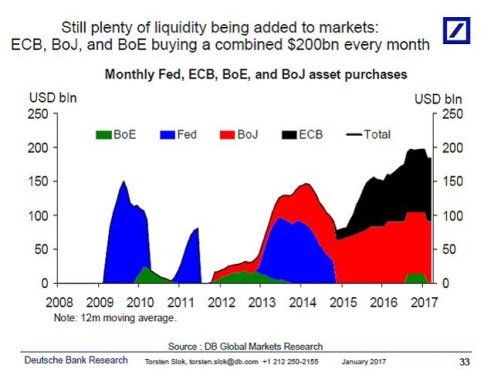

This vast expansion of stimulus in year Eight of “expansion/recovery” is an unprecedented extreme: does anyone seriously believe you can stop this flood and markets will “normalize”?

This essay was first published on peakprosperity.com under the title The Inescapable Reason Why the Financial System Will Fail.

Click here to read Part 2 of this report (free executive summary, enrollment required for full access)

My new book Money and Work Unchained is $9.95 for the Kindle ebook and $20 for the print edition.

Read the first section for free in PDF format.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

Source Article from http://feedproxy.google.com/~r/blacklistednews/hKxa/~3/B4mkOyMuBbs/M.html

Related posts:

Views: 0

Posted in

Posted in  Tags:

Tags: