RSS Feed

RSS Feed

October 17th, 2023

October 17th, 2023  Awake Goy

Awake Goy Treasuries Pain Can Get Much Worse, Term Premium Dynamics Show

By Garfield Reynolds, Bloomberg Markets Live reporter and strategist

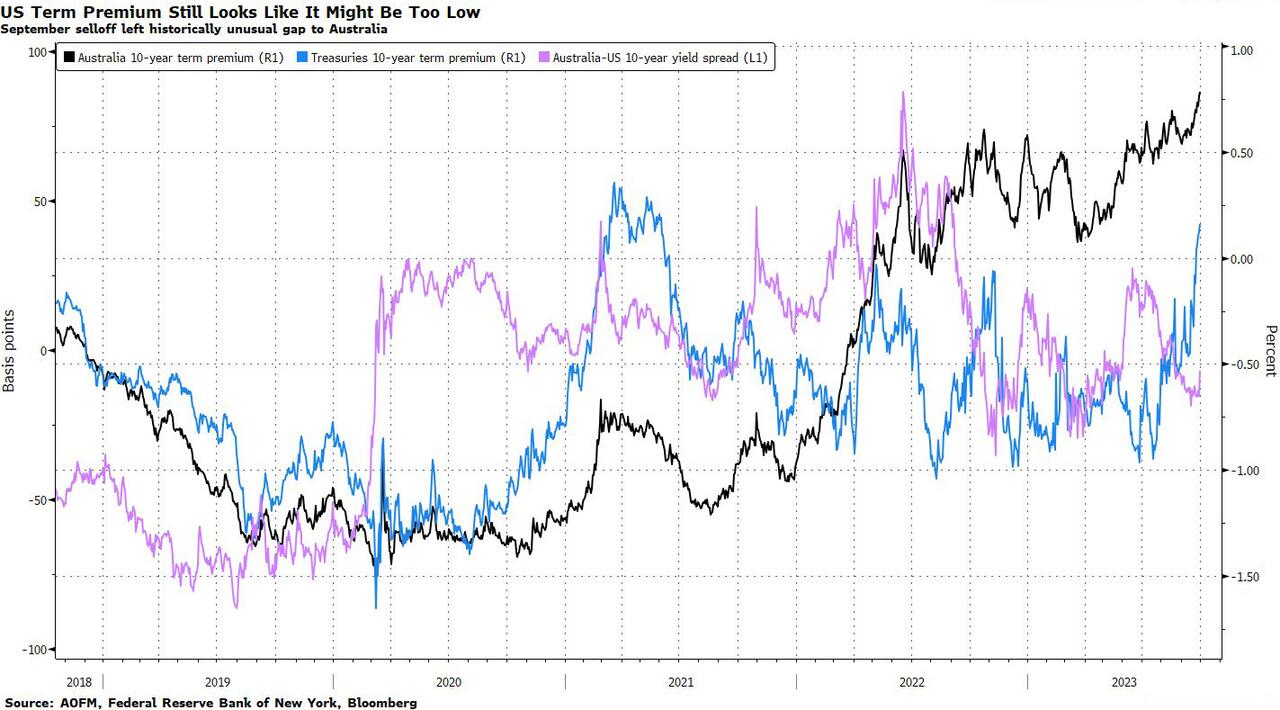

Treasuries’ recent slump owed plenty to the return of the so-called term premium as investors became more concerned about the risks of holding longer-dated debt. Even as US bonds get some help from geopolitical uncertainty, there’s plenty of scope for yields to march considerably higher on the same dynamics that helped drive September’s spike.

For one thing there’s little chance that the supply outlook is going to improve noticeably, no matter how the Middle East conflict and the US House speaker situation are resolved. For another, an examination of the relative yields for Australian and US debt signals there’s potential that US term premiums have further to go to.

Australia’s 10-year term premium has tended to align closely with the US gauge, but it’s been going through a relatively rare period since the pandemic with the two diverging. At first, it was the US term premium that swelled, perhaps representing the impact of extreme QE or lingering liquidity concerns after Treasuries froze as the pandemic broke out. That script flipped from early 2022 as the Fed started what would prove to be a far more aggressive hiking cycle than the RBA.

Still, as inflation slows in both economies and traders anticipate and end to rate hikes, that term premium gap closed dramatically even as September’s selloff drove steep losses for both Treasuries and Aussie bonds. Term premiums are tough enough to measure, let alone predict, but there’s a case to be made that one potential guide for the way for this to develop would be for the US term premium to close much of the remaining spread to Australia, which stood at about 60bps at the end of last month.

Tyler Durden

Tue, 10/17/2023 – 07:45 Source

Views: 0

Posted in

Posted in  Tags:

Tags: