RSS Feed

RSS Feed

September 8th, 2023

September 8th, 2023  Awake Goy

Awake Goy In retrospect, it’s surprising that it took so long.

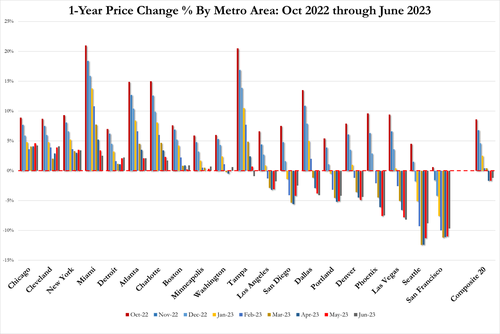

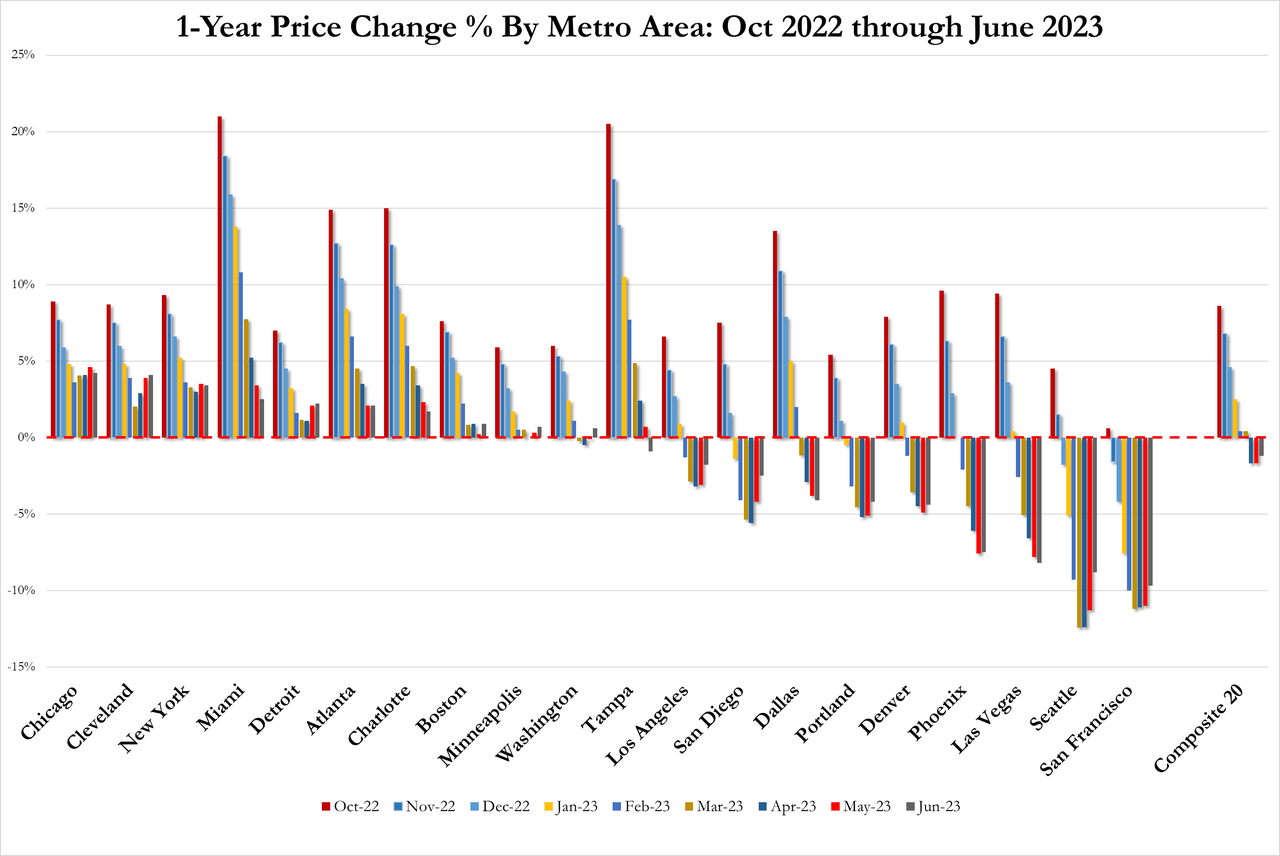

With Case-Shiller reporting that the nation’s worst-by-far (not to mention feces-covered) real-estate market is that of San Francisco, where prices have seen annual declines for the past 8 months, half of which have seen double-digit drops…

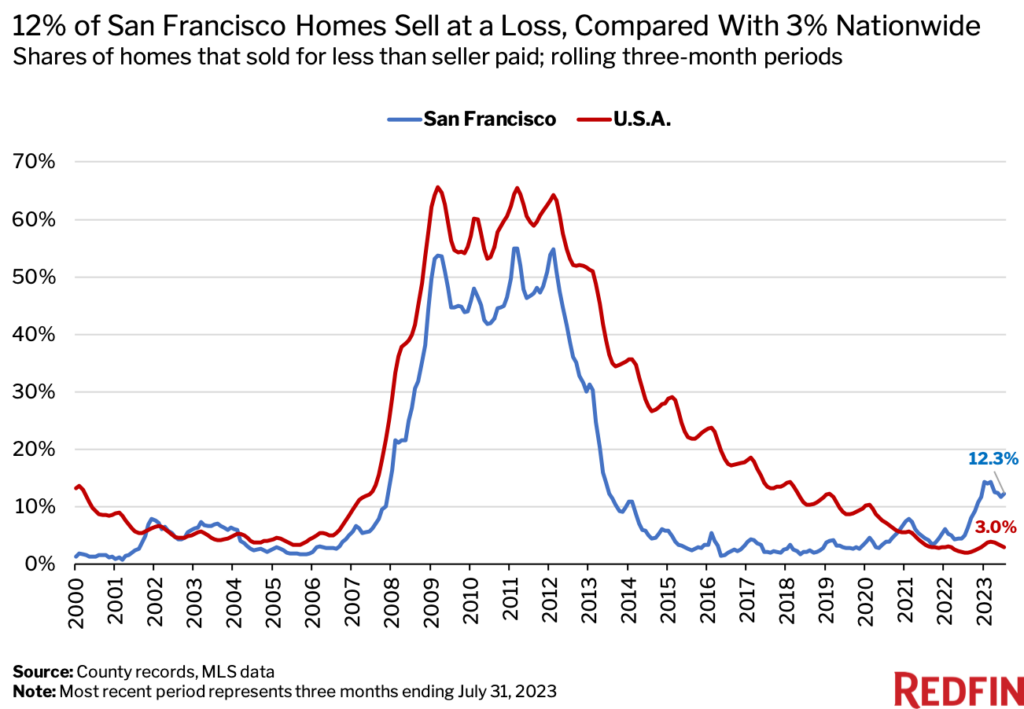

…. overnight RedFin reports more bad news for those unlucky enough to be living in the socialist utopia that is San Francisco: home sellers in this liberal bastion are four times more likely than the average U.S. home seller to take a loss, as the Bay Area metro reels from an outsized drop in home prices. In fact, according to the report, the typical San Francisco seller who takes a loss sells their home for $100,000 less than they bought it for. And when they do, they have to walk on shit-covered streets, through crowds of homeless, to buy another home one which they pray won’t be burgled in the near future because, well, good luck calling cops in San Fran.

Here are the details from Redfin:

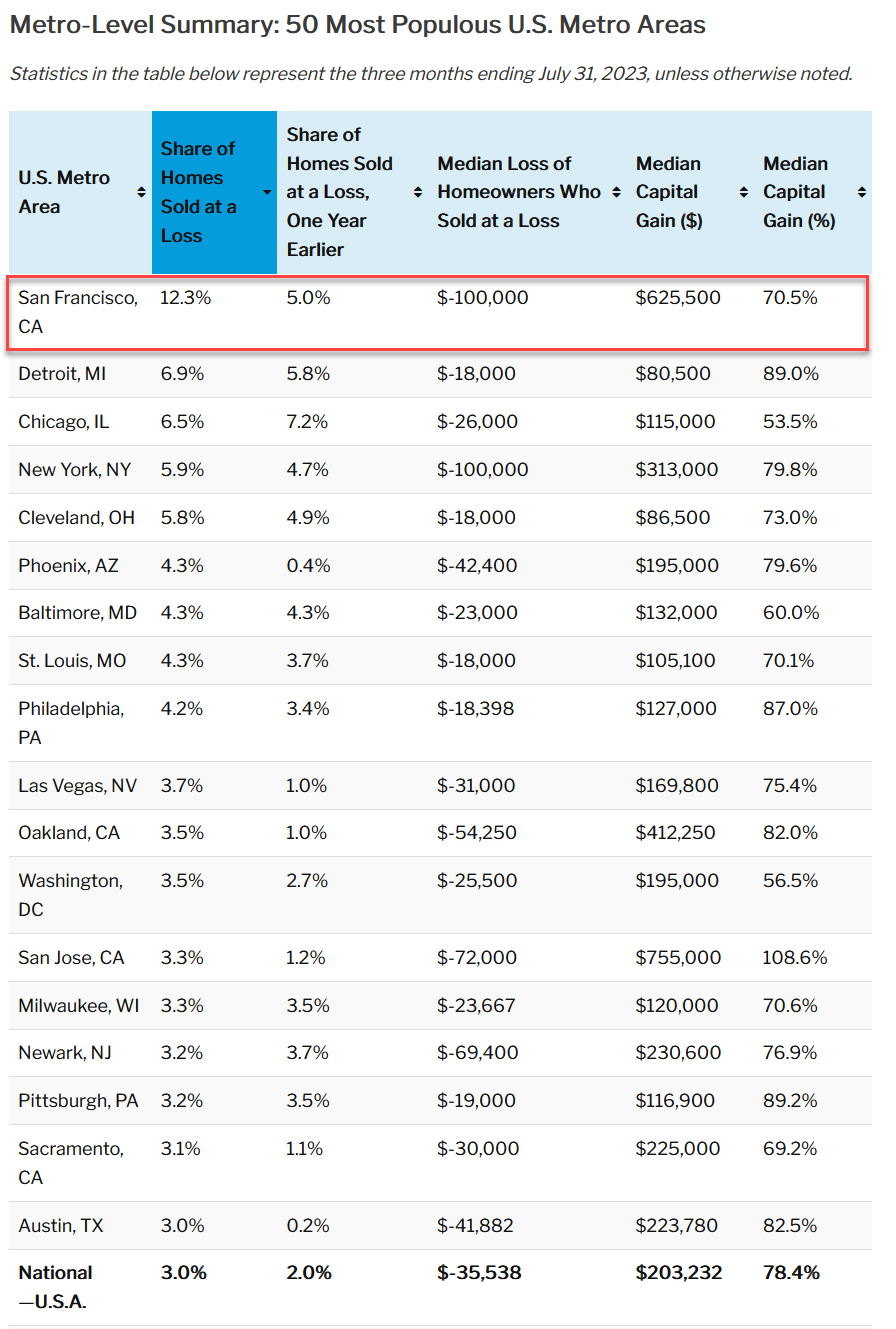

Roughly one of every eight (12.3%) homes that sold in San Francisco during the three months ending July 31 was purchased for less than the seller bought it for, up from 5% a year earlier. That’s a higher share than any other major U.S. metro and is quadruple the national rate of 3%.

Next came Detroit (6.9%), Chicago (6.5%), New York (5.9%) and Cleveland (5.8%).

In San Francisco, which tied with New York for the largest median loss in dollar terms, the typical homeowner who took a loss sold their home for $100,000 less than they bought it for. Nationwide, the typical homeowner who sold their home for less than they bought it for lost $35,538.

Homeowners were least likely to sell at a loss in San Diego, Boston, Providence, RI, Kansas City, MO and Fort Lauderdale, FL. In each of those metros, roughly 1% of homes sold for less than the seller originally paid.

* * *

Turning back to San Francisco, just because it’s both terrifying and amusing to watch a formerly great city implode under the weight of Soros-funded DAs, here home sellers were most likely to lose money because the region has experienced outsized home-price declines. It was one of the first markets to see prices sink when high mortgage rates triggered a slowdown in the housing market last year. By April 2023, San Francisco’s median home sale price was down a record 13.3% year over year, more than triple the nationwide drop of 4.2%. As of July, it was down just 4.3% year over year to $1.4 million, but that compared with a national gain of 1.6%. The total value of homes in San Francisco has fallen by roughly $60 billion since last summer, a separate Redfin analysis found.

Prices in the Bay Area have fallen fast for a few reasons:

- First, it’s home to the most expensive real estate in the country, meaning housing costs had a lot of room to come down. It has also been hit hard by layoffs in the technology sector.

- Additionally, it’s not as popular as it once was; remote work has allowed scores of people to relocate to more affordable areas.

Next, read the following sentence and see if you can spot the common thread:

“San Francisco, Detroit, Chicago and New York, which top the list of metros where home sellers are most likely to take a loss, all rank among the top 10 metros Redfin.com users are looking to leave.”

If you said these are all traditionally Republican-controlled bastions… you failed.

“Some condos in the Bay Area are now worth less than their owners bought them for in 2018 and 2019, in part because commuting from Oakland and other outlying areas into downtown San Francisco isn’t really a thing anymore,” said local Redfin Premier real estate agent Andrea Chopp, who focuses on Oakland and other East Bay neighborhoods. “There are buyers out there, but they’re a lot more cautious and picky than they were when mortgage rates were low. The Bay Area housing market was unsustainable before, so this correction is probably healthy, but the unfortunate thing is prices remain unaffordable for a lot of people—especially with rates now above 7%.”

But while the liberal bastion of San Francisco is now officially America’s worst city, the vast majority of U.S. home sellers are still reaping gains, especially those

Even though home prices have fallen from their peak, a majority of home sellers are still reaping significant financial gains. Nationwide, 97% of home sellers sold for a profit during the three months ending July 31, with the typical home that sold going for 78.4% ($203,232) more than the seller bought it for.

Today’s home sellers are making money despite an ongoing housing downturn in part because a scarcity of homes for sale is fueling bidding wars and propping up home values. Most people who bought when home prices peaked would lose money if they sold now, so they’re not selling. Many of the homeowners who are selling today have owned their homes for long enough to make a profit regardless of month-to-month fluctuations in housing values.

In Boise, ID, Redfin Premier agent Shauna Pendleton has clients who will likely have to take a $100,000 loss on their home because they’re selling it after only about a year. They’re moving back to Seattle because their employer is requiring them to return to the office. Pendleton noted that it’s not common for homeowners to sell at a loss in Boise, but when it does happen, it often involves homes selling for upwards of $750,000.

More in the full Redfin report available here.

Related posts:

Views: 0

Posted in

Posted in  Tags:

Tags:

{kind=link}

{kind=link}

{kind=link}